Unsecured Loan Agreement

This loan agreement (the “Agreement”) is dated Agreement date and is made by and between:

Borrower (Name), a Borrower company jurisdiction corporation, as borrower (the “Borrower”); and

Lendor (Name), a Lender company jurisdiction corporation, as lender (the “Lender”),

who make this Agreement on the following terms:

Subject of the Agreement

The Lender agrees to make loans (individually an “Advance” and collectively the “Loan”) to the Borrower for its working capital needs. Each Advance and the amount of the Loan outstanding shall be denominated in Loan currency and the maximum amount of the Loan advanced and not repaid at any time shall not exceed Maximum loan amount (“Maximum Loan Amount”).

This Agreement shall remain effective for Agreement duration up to Agreement termination date. This Agreement is renewable upon mutual agreement.

The Borrower may repay all or any portion of the Loan at any time or from time to time, provided that the unpaid balance of each Advance shall be due and payable in full no later than Advance repayment duration from the date of such Advance or the termination of this Agreement, whichever comes first (each such date being a “Termination Date”). Amounts repaid may not be re-borrowed.

Loan Drawdown

The Borrower may receive the Loan in one or more Advances upon delivery of an Advance Request in the form attached to this Agreement as Exhibit 1 no later than Advance request notice period before the date of the requested Advance (the “Advance Date”) as long as, after giving effect to the requested Advance, the amount of the Loan advanced and not repaid will not be greater than the Maximum Loan Amount.

As used in this Agreement, “Business Day” means a day on which banks in Banking jurisdiction are open for dealings in Loan currency in the interbank market.

Interest

The Borrower shall pay accrued interest (as determined in accordance with Section 3.2 of this Agreement) on the Loan amount of each Advance upon full repayment of the Advance on the respective Termination Date.

Interest on the total amount of each Advance shall accrue from and including the first day of such Advance to but excluding the repayment day of such Advance. The rate of interest applicable to an Advance shall be equal to Interest rate percentage% per annum.

Interest shall be calculated on the number of days elapsed over a year of Interest calculation year basis days.

Representations and Warranties of the Borrower

The Borrower represents and warrants to the Lender that:

The Borrower

is a corporation duly organized and validly existing under the laws of Borrower company jurisdiction, and

has the corporate power and authority to execute, deliver and perform its obligations under this Agreement.

The transactions contemplated by this Agreement

have been duly authorized by all requisite corporate and, if required, board action and

will not violate (a) any material provision of any law, rule or regulation, or the articles of incorporation of the Borrower, or (b) any order of any governmental authority.

This Agreement has been duly executed and delivered by the Borrower and constitutes the legal, valid, and binding obligation of the Borrower, enforceable against it in accordance with its terms.

No action, consent or approval of, or registration or filing with or any other action by any governmental authority is or will be required in connection with this Agreement.

Covenants of the Borrower

The Borrower covenants with the Lender that, so long as this Agreement shall remain in effect and until any obligation of the Lender to make Advances hereunder shall have terminated and the Loan and all other sums due to the Lender under this Agreement have been paid in full, it shall furnish the Lender prompt written notice of any Default or Event of Default, which notice shall specify the nature and extent thereof and the corrective action (if any) taken or proposed to be taken with respect thereto.

Defaults and Events of Default

The occurrence of any of the following events shall constitute an “Event of Default”:

Any representation or warranty made or deemed made in or in connection with this Agreement proves to have been false or misleading in any material respect when so made or deemed made and such misrepresentation continues unremedied for Default cure period days after the Borrower’s receipt of written notice thereof from the Lender; or

The Borrower fails to make when due any payment required under this Agreement and such failure continues unremedied for Default cure period days after the Borrower’s receipt of written notice thereof from the Lender; or

The Borrower fails to perform any other covenant, condition, or agreement set forth in this Agreement and such failure continues unremedied for Default cure period days after the Borrower’s receipt of written notice thereof from the Lender; or

An Act of Insolvency occurs in relation to the Borrower; or

The Borrower becomes bankrupt or insolvent as defined in any bankruptcy or insolvency law applicable to it; or

The Borrower fails to pay or is otherwise unable to pay its debts as they become due.

As used in this Agreement, “Default” means any event or circumstance which, with notice and/or the passage of time, would constitute an Event of Default, and “Act of Insolvency” means the occurrence of any of the following events:

The filing of a voluntary petition in bankruptcy or insolvency or a petition for reorganization under any bankruptcy or insolvency law by the Borrower or the admission by the Borrower that it is unable to pay its debts as they become due; or

The entering of an order, judgment or decree by any court of competent jurisdiction, on the application of a creditor adjudicating the Borrower as bankrupt or insolvent or approving a petition seeking reorganization or appointing a receiver, trustee, liquidator, administrative receiver, administrator, compulsory manager or other similar officer over all or a substantial part of the Borrower’s assets, and such order, judgment or decree continuing unstayed and in effect for a period of Insolvency order duration days; or

The consent to an involuntary petition in bankruptcy or the failure to vacate, within Involuntary petition cure period days from the date of entry thereof, any order approving an involuntary petition by the Borrower.

Liability of the Parties; Dispute Resolution

The obligations of the Borrower hereunder are unsecured.

This Agreement is governed by the laws of Governing jurisdiction law and each Party submits to the jurisdiction of the courts of Governing jurisdiction state in connection with the Agreement. Each Party shall be liable for failure to perform or improper performance of this Agreement in accordance with applicable laws of Governing jurisdiction law.

Any disputes or differences which cannot be amicably resolved by the Parties within Dispute resolution period days after the date of occurrence thereof shall be settled by the courts of Governing jurisdiction state, in accordance with applicable laws of Governing jurisdiction law.

Miscellaneous

This Agreement may be extended by mutual consent of the Parties, provided that any amendment complies with all applicable legal requirements. The rights and obligations under this Agreement cannot be transferred or assigned by either Party. The Lender consents to the assumption of this Agreement and the Borrower’s rights and obligations hereunder by any person that becomes the legal successor of the Borrower by operation of law. No person other than the Lender and the Borrower shall have any rights under or by virtue of this Agreement.

Any amendments hereto shall be executed in writing and signed by both Parties.

This Agreement may be executed in any number of counterparts, and this has the same effect as if the signatures on the counterparts were on a single copy of the Agreement.

There is no express or implied intention for this Agreement to benefit any third party, and nothing contained in this Agreement is intended, nor shall anything herein be construed, to confer any rights, legal or equitable, in any person other than the Borrower.

A person who is not a party to this Agreement has no right under the agreement to enforce or to enjoy the benefit of any of its terms. The consent of any person who is not a party to this Agreement is not required to rescind or vary this Agreement at any time.

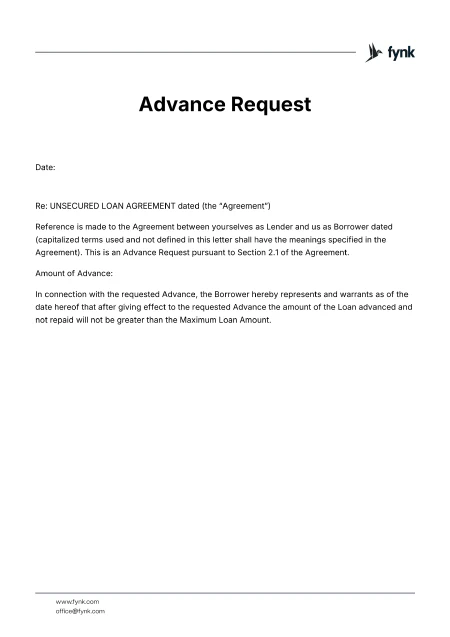

Advance Request

Borrower (Name)

Date: Advance request date

Lendor (Name)

Re: UNSECURED LOAN AGREEMENT dated Agreement date (the “Agreement”)

Reference is made to the Agreement between yourselves as Lender and us as Borrower dated Agreement date (capitalized terms used and not defined in this letter shall have the meanings specified in the Agreement). This is an Advance Request pursuant to Section 2.1 of the Agreement.

Amount of Advance: Advance amount currency and value

In connection with the requested Advance, the Borrower hereby represents and warrants as of the date hereof that after giving effect to the requested Advance the amount of the Loan advanced and not repaid will not be greater than the Maximum Loan Amount.