Amortization in contract clauses refers to the process of gradually reducing a debt or an asset's book value over a specified period, typically through regular payments or expense allocations. This clause outlines how financial obligations or asset costs are spread out over time, providing clarity on payment schedules and tax implications.

Table of Contents

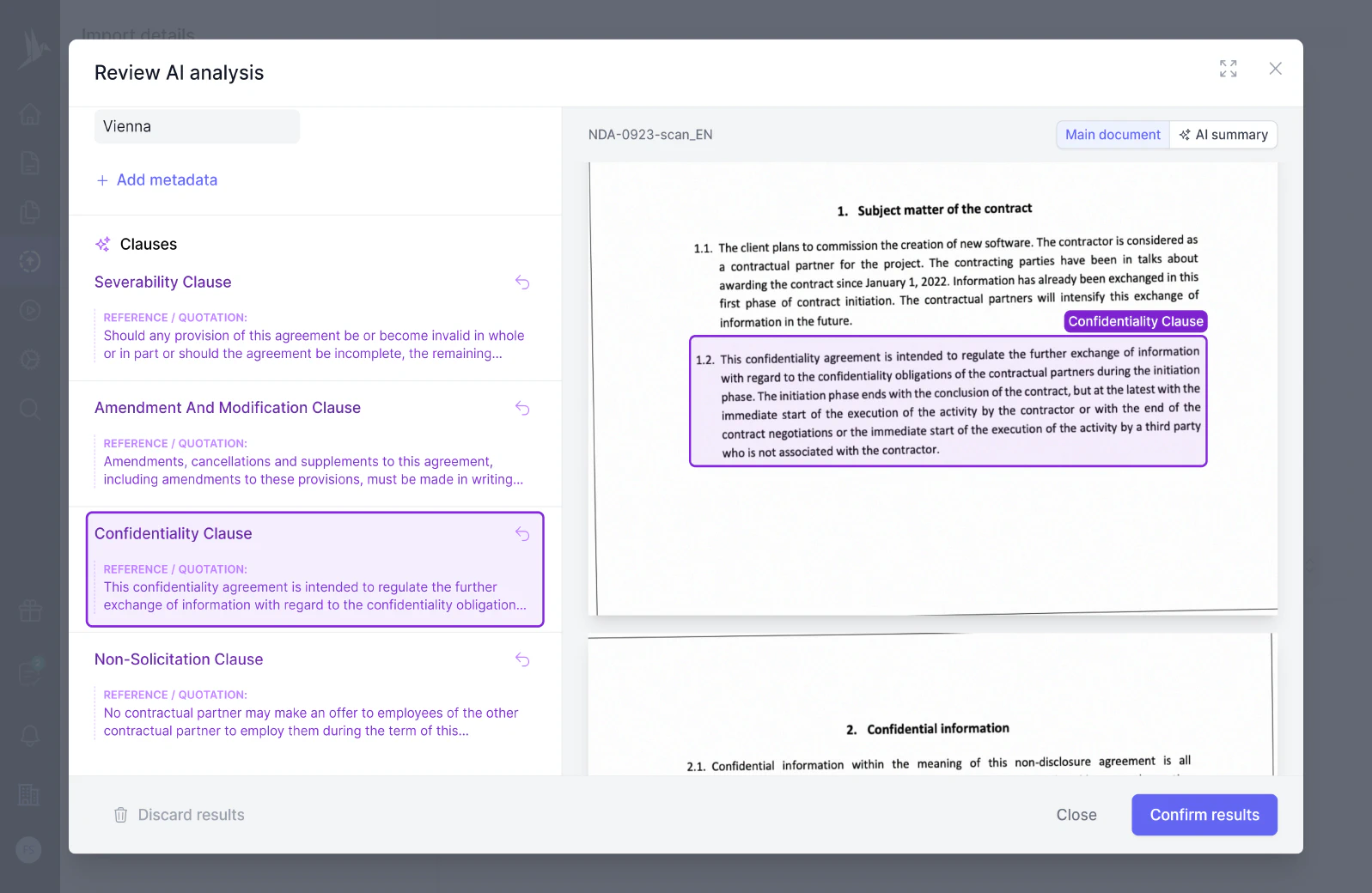

Want to automatically extract clauses from your contracts?

Amortization Payments. In addition to all other obligations under this Note, the Borrower shall make the following amortization payments (each an “Amortization Payment”) in cash to the Holder towards the repayment of this Note, as provided in the following table:

With respect to the third Amortization Payment originally due on August 15, 2022 (the “Third Amortization Payment”), the Company may notify the Holder on or before August 15, 2022, that the Company is electing to extend the due date of the Third Amortization Payment to September 15, 2022 (the “Third Amortization Payment Extension”) as further provided herein. If the Company exercises the Third Amortization Payment Extension, then the Third Amortization Payment shall be due on September 15, 2022 and the Company shall pay $4,440.00 (the “Third Amortization Payment Extension Fee”) to the Holder on or before August 15, 2022. For the avoidance of doubt, the Third Amortization Payment Extension shall not affect the due date of any other Amortization Payment and the Third Amortization Payment Extension Fee shall not reduce the amounts owed under the Note. The Company shall not be permitted to exercise the Third Amortization Payment Extension if an Event of Default occurs under the Note.”

EBITDA is net income, as defined by U.S. GAAP, plus preferred dividends, interest expense, including amortization of financing costs, depreciation and amortization, net amortization of acquired above and below market lease revenue, loss on impairment, and impairment of assets held for sale.

Depreciation and amortization attributable to operating expenses reflects depreciation and amortization related to our corporate and administrative offices along with internet technology (IT) related items and intangibles.

Amortization of capitalized implementation costs represents amortization of upfront costs to implement new customer contracts under our SaaS and hosted revenue model, as well as amortization of contract acquisition costs.

Amortization of internally-developed software. Included in our GAAP presentation of cost of revenue and operating expenses, amortization of internally-developed software reflects non-cash expense for software developed or obtained for internal use. We exclude these expenses from our non-GAAP measures because we believe they are not indicative of our core operating performance.

Amortization of purchased intangibles. Included in our GAAP presentation of gross margin and operating expenses is amortization of purchased intangible assets. We believe amortization of acquisition-related intangible assets, such as amortization of costs associated with an acquired company’s research and development efforts, trade names and customer relationships, are items arising from pre-acquisition activities and determined at the time of an acquisition. Although these intangible assets are continually evaluated for impairment, amortization of purchased intangibles is a static expense and not typically affected by operations during any particular period.

Amortization of contract acquisition costs - ASC 606 initial adoption. Upon adoption of ASC 606 using the modified retrospective approach, we capitalized approximately $3.3 million of previously expensed sales commissions from 2015, 2016 and 2017. Amortization of these amounts are included in our GAAP presentation as sales and marketing expense. We believe the non-cash amortization expense is not related to or indicative of our ongoing operating performance.

Adjustments to 2023 EPS include estimated impacts of approximately $0.40 per share for acquisition-related amortization, as well as $0.20 per share for restructuring, M&A and amortization expense related to acquired backlog (approximately $9 million pre-tax).

Amortization is an accounting and financial concept that involves gradually writing off the initial cost of an asset over a period of time. It is used for two main purposes: the systematic reduction of debt and the allocation of the cost of an intangible asset over its useful life. In the context of a loan, amortization refers to the process of paying off a debt over time through regular payments. For intangible assets, it involves spreading out the cost of an asset, such as a patent or trademark, over its productive life.

When should I use Amortization?

Amortization should be used when you need to systematically reduce a financial obligation or when you are allocating the cost of an intangible asset. It is typically used in the following scenarios:

Loans: To determine the payment schedule for the principal and interest over the loan term.

Intangible Assets: To allocate the cost of an asset over its useful life, helping to reflect its value accurately on financial statements.

How do I write Amortization?

Writing amortization involves creating a schedule that outlines each payment’s allocation towards the principal and interest, or the allocation of an asset’s cost over its useful life. Here’s a general guide on how to write amortization:

For Loans:

Determine the loan amount, interest rate, and loan term.

Create a table or schedule showing each period’s payment, breaking it down into principal and interest components.

Example:

Period

Payment

Principal

Interest

Balance

1

$500

$300

$200

$9,700

2

$500

$305

$195

$9,395

…

…

…

…

…

For Intangible Assets:

Identify the asset’s cost and its useful life.

Use a straight-line method to divide the cost evenly over the asset’s life.

Example:

Amortization Expense (Yearly) = Total Cost / Useful Life

If a patent costs $10,000 and has a useful life of 5 years:

$10,000 / 5 = $2,000 annual amortization expense.

Which contracts typically contain Amortization?

Contracts that typically contain amortization include:

Loan Agreements: Most loan agreements, especially mortgages and auto loans, contain amortization schedules to detail the repayment terms.

Lease Agreements: Capital leases may use amortization to allocate the cost of a leased asset over its lease term.

Intellectual Property Licenses: Contracts involving intellectual properties, like patents and copyrights, often include amortization terms to manage the cost allocation of the assets involved.

More Clauses from the Library

Dive deeper into the world of clauses and learn more about these other clauses that are used in real contracts.

The Annual Bonus Eligibility clause outlines the conditions under which an employee qualifies for a yearly bonus, typically based on factors like individual performance, departmental goals, or overall company success. It specifies any criteria, such as employment duration or achievement of specific milestones, that must be met for the employee to receive the bonus.

The Annual Leave clause outlines the entitlement of employees to take paid time off from work each year for rest and relaxation, specifying the number of days or weeks available and any conditions for taking this leave. It may also include details about the process for requesting leave, notice requirements, and provisions for carrying over unused leave to subsequent years.

The "Annual Vacation" clause outlines the entitlement of employees to a specified number of vacation days each year, during which they continue to receive regular compensation. It typically includes provisions on how vacation time is accrued, the process for scheduling, and any limitations on carrying over unused days to subsequent years.

15 example clauses

Analyze your contracts. Extract important clauses.

<

Try our AI contract analysis and extract important clauses and information from existing contracts.