Poison pill

A poison pill is a strategy used by a company to discourage hostile takeovers by making its stock less attractive to potential acquirers. It typically involves the issuance of additional shares or rights to existing shareholders, diluting the value and control of the potential acquirer.

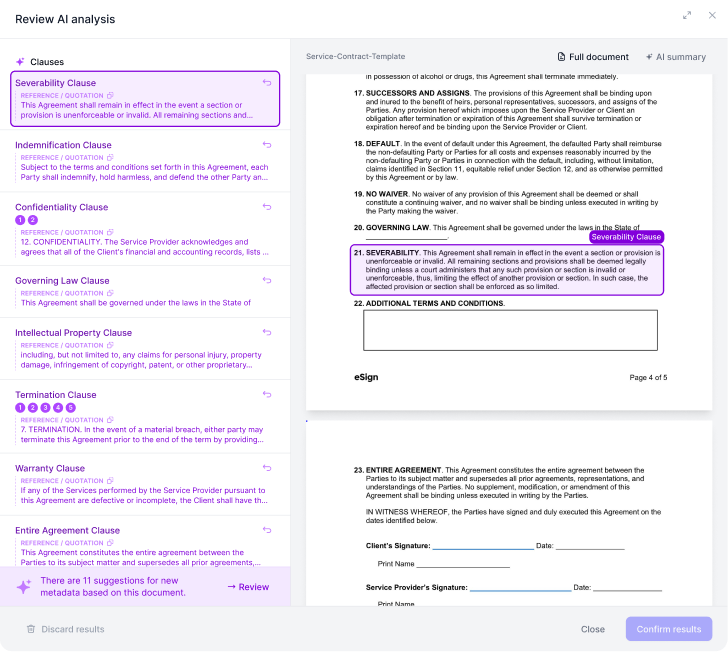

Analyze your contracts. Extract important clauses.

Try our AI contract analysis and extract important clauses and information from existing contracts.

Save your favourite clauses

Insert directly with a single click

Upload preferred precedents

Sample Poison pill clauses

Concerned Shareholders of Rocky Mountain Comment on Dubiously Timed Board Decision to Rescind Poison Pill on Eve of Annual Meeting

After AB Value’s Years of Advocating for Such a Decision, which the Board Ignored, the Recent Announcement is Only in Response to Shareholder Pressure

The Board’s Refusal to Seek Shareholder Approval for the Poison Pill Redemption Proposal Suggests that the Board Cannot be Trusted

No Assurances Preventing the Board from Reinstating a Poison Pill Without Shareholder Approval

Unlike the Board, the Concerned Shareholders of Rocky Mountain Included Shareholder Proposal to Redeem the Poison Pill

The Concerned Shareholders of Rocky Mountain note that until now, the Board had consistently decided to keep this poison pill on its books every day for the past 22+ years. With the contested election at the 2021 Annual Meeting looming, the Concerned Shareholders of Rocky Mountain do not believe the Board’s sudden, convenient change of heart to be an authentic demonstration of proper corporate governance. This timing suggests that certain incumbent Board members have shown once and for all that their priority is self-preservation over, and at the expense of, maximizing shareholder value.

WESTFIELD, N.J.–(BUSINESS WIRE)–AB Value Management LLC (collectively with its affiliates, “AB Value”), and the other participants in this solicitation (collectively with AB Value, the “Concerned Shareholders of Rocky Mountain”) representing approximately 14.70% of the outstanding shares of Rocky Mountain Chocolate Factory, Inc. (the “Company”), today commented on the Company’s desperate last-minute rescindment of its poison pill (which originated in the 1990s),1 merely four days before the Company’s 2021 Annual Meeting of Shareholders (the “2021 Annual Meeting”) scheduled for October 6, 2021.

The Concerned Shareholders of Rocky Mountain also noticed that the Company’s furtive Saturday night announcement noticeably lacked any commitment from the Board preventing it from unilaterally adopting another unjustifiable long-term pill following the 2021 Annual Meeting. To avoid such a disingenuous maneuver, the Concerned Shareholders of Rocky Mountain intend to bring their proposal to request that the Board redeem any poison pill previously issued and not adopt or extend any poison pill, unless submitted to a shareholder vote within 12 months of such adoption (such proposal, the “Poison Pill Redemption Proposal”) at the 2021 Annual Meeting. No such policy has been adopted by the Company. Prior to rescinding the poison pill Saturday evening, the Board had refused to even acknowledge the Concerned Shareholders of Rocky Mountain’s Poison Pill Redemption Proposal in the Company’s proxy statement. To date, the Board has not taken a position on the Poison Pill Redemption Proposal, yet has refused to allow shareholders to vote on the proposal using the Company’s proxy card.

Each of the Directors was a member of the Board at the time ASA adopted the Poison Pill, and participated in and authorized the adoption of the Pill.

The Poison Pill gives common shareholders the right to acquire one additional ASA common share at $1.00 per share for each common share owned, but denies that right to shareholders who acquire beneficial ownership of more than 15% of ASA after the adoption of the Pill.

ASA’s Poison Pill is discriminatory and specifically targeted at Saba. In its January 2, 2024 press release announcing the Pill, ASA conceded that the Board adopted the Pill “in response to the rapid and significant accumulation of ASA shares by Saba Capital Management, LP.”

Source

Eagle Bulk Shipping Inc.We struggle to see how the poison pill truly accomplishes the Company’s stated goal of avoiding “abusive tactics” and are concerned with where the share repurchase and poison pill leave us as well as the Company’s other remaining shareholders. To this point, we note that it is also peculiar that the Board is only now adopting this poison pill (which is triggered at 15%) given the fact that Oaktree was long permitted to maintain its significant 28% stake without a similarly threatening response from the Board. Oaktree is a $164 billion enterprise with control positions in multiple public shipping companies. They have the knowledge and means to acquire the Company, but no poison pill was in place to prevent them from doing so.

Source

KOHLS Corp (KSS)Kohl’s Corp. is taking a ‘poison pill.”

The department store retailer said it is rejecting the takeover offers it received, saying they undervalue the business. It also said it has adopted a shareholder rights plan, commonly knowns as a “poison pill,” to avert a hostile takeover of its business. The plan, scheduled to expire in February 2023, will become exercisable if any stockholder acquires 10% beneficial ownership, or 20% in the case of passive institutional investors.

Source

KOHLS Corp (KSS)Macellum Advisors, of New York City, announced early Thursday a slate of 10 board nominees including several with experience as retail executives. Jonathan Duskin, the managing partner of Macellum, which holds about 5% of the stock in Kohl’s (NYSE: KSS), pilloried the Kohl’s board for rejecting takeover offers of $64 to $65 per share and adopting a “poison pill” shareholder rights plan.

On October 17, 2022, Barnwell Industries, Inc. announced the execution of a Tax Benefits Preservation Plan, commonly known as a “poison pill” but with a low 4.95% ownership trigger. The Barnwell board approved the poison pill by a 4-3 vote, with CEO Alex Kinzler, Phil McPherson, Peter O’Malley and Francis Kelly leading the initiative and voting in favor. The Barnwell board implemented the poison pill despite the rejection by shareholders of the board’s blank-check preferred stock proposal at its recent 2022 annual meeting of shareholders, which clearly indicated shareholders’ opposition to a poison pill. The poison pill is also another afront to the “Cooperation and Support Agreement” signed by Barnwell with MRMP-Managers on January 27, 2021. Although Barnwell’s net operating losses have existed for many years, the potential loss of the NOLs has not been mentioned as a risk factor in any of Barnwell’s SEC filings during the past three years. However, the standstill provisions and stock ownership limitations that bind MRMP and protect the Barnwell board under the “Cooperation and Support Agreement” expire in connection with Barnwell’s next annual meeting of shareholders, at which time MRMP and other shareholders would have no restriction on buying Barnwell shares in the absence of an anti-shareholder “poison pill.” The board’s misguided approach to dealing with MRMP and other shareholders leaves MRMP no choice but to run a proxy contest at Barnwell’s 2023 annual meeting of shareholders, which is fast-approaching.

On September 22, 2020, four days after Ms. Benson resigned from the Board, the Company announced the adoption, without shareholder approval, of a Poison Pill (defined below) that would prohibit shareholders from acquiring more than 9.8% of the Company’s Common Stock. The Company stated that it was adopting the Poison Pill to “protect stockholder interests” as it explored converting to a REIT. The Poison Pill contained an “acting in concert” provision that sought to aggregate the holdings of shareholders working together for purposes of triggering the poison pill.

On November 23, 2020, the Company responded to Oasis’ letter regarding the Poison Pill and confirmed that the basic activities and communications amongst shareholders outlined by Oasis would not trigger the Poison Pill.

Source

WisdomTree, Inc. (WT)The move by ETFS Capital and Lion Point prompted WisdomTree to adopt a short-term poison pill later that month, barring shareholders from holding more than 10% of the company’s common stock until after its 2022 annual meeting.

On July 20, 2023, Paragon submitted a request for an exemption under OPT’s NOL poison pill, as contemplated by Section 27 of the poison pill, subject to the condition that Paragon would not exceed ownership of 19.9% of OPT’s outstanding shares of common stock. Paragon made the request on the basis that its increased ownership “will not limit or impair the availability to [OPT] of the Tax Benefits” pursuant to Section 27 of the poison pill. OPT did not respond to Paragon’s exemption request until October 12, 2023.

Source

Capitol Series TrustPOISON PILLS & GOLDEN PARACHUTES

The Firm believes that the shareholders of a corporation should have the right to vote upon decisions in which there is a real or potential conflict between the interests of shareholders and those of management. As such, the Firm will vote in favor of shareholder proposals requesting that a corporation submit a “poison pill”2 for shareholder ratification. The Firm will examine, on a case-by-case basis, shareholder proposals to redeem a poison pill and management proposals to ratify a poison pill. Also, on a case-by-case basis, the Firm will vote in favor of proposals requiring that “golden parachute”3 proposals be submitted for shareholder approval. The Firm will vote against a poison pill or golden parachute that was not approved by shareholders.

Source

Capitol Series Trust“Poison pill” is an antitakeover measure stipulating that shareholders on the receiving end of a hostile takeover may buy shares in their own company at a price below fair market value. Once the acquisition is complete, the provision allows these same shareholders to buy more shares in the new company for below market value. This forces shareholders in the acquiring company to suffer a devaluation and dilution of their own shares. This is done to discourage hostile takeovers among the shareholders of the acquiring companies. It is important to note that a poison pill need not use both of these tactics; sometimes it utilizes only one or the other.

What is a Poison Pill?

A poison pill is a mechanism that companies use to prevent or deter hostile takeovers. It typically allows existing shareholders the right to purchase additional shares at a discount, diluting the ownership interest of a potential acquirer and making the takeover more expensive and difficult to achieve. Poison pills are a form of defense for a company’s board of directors to protect the interests of current shareholders and maintain control over the company’s strategic direction.

When should I use a Poison Pill?

A poison pill should be used when there is a risk of a hostile takeover, where an acquirer attempts to gain control of a company by purchasing a majority of its shares without the consent of the board of directors. It is generally employed as a defensive measure to ensure that the company has the opportunity to negotiate terms that are favorable to existing shareholders or to seek alternative suitors. Companies should consider implementing a poison pill when there is an indication of unwanted acquisition attempts or when the board believes that the company’s long-term strategic plans are threatened by such takeovers.

How do I write a Poison Pill?

Writing a poison pill involves drafting a shareholder rights plan that specifies the details of how and when the rights will be triggered. It requires careful legal drafting to ensure compliance with relevant securities laws and regulations. The key components typically include:

- Trigger Event: Define the event that activates the poison pill, such as when a single shareholder acquires a certain percentage of shares (usually between 10-20%).

- Rights Distribution: Outline the distribution of rights to existing shareholders, allowing them to purchase additional shares at a discount if the trigger event occurs.

- Exclusion Clauses: Specify any exemptions or exclusions, such as allowing friendly takeovers or certain insider purchases.

- Duration and Amendments: Establish the lifespan of the rights plan and the conditions under which it may be amended or terminated.

It’s essential to consult with legal and financial advisors when drafting a poison pill to tailor it specifically to the company’s needs and ensure it aligns with shareholder interests.

Which contracts typically contain a Poison Pill?

Poison pills are typically found within shareholder rights plans, which are contracts that the company adopts to outline the terms and conditions of the rights issuance in the event of a triggering event. These plans are often accompanied by amendments to the company’s charter or bylaws to enforce the provisions of the poison pill.

While poison pills themselves are not traditionally part of standalone contracts, they influence various corporate agreements and can be a consideration in merger and acquisition contracts, investment agreements, and even employment contracts with key executives where change-in-control provisions are relevant.

More clauses from the library

See allPreamble

The preamble of a contract is an introductory section that outlines the purpose and intent of the agreement, often providing context and background information relevant to the parties involved. It serves to set the stage for the contractual terms that follow, ensuring that all parties have a mutual understanding of the underlying reasons for the contract.

7 example clauses

Prepayment

A prepayment clause outlines the terms under which a borrower can pay off a loan or portion of it before its due date without facing penalties. This clause often specifies any conditions or fees associated with early payments, helping borrowers manage their financial obligations more flexibly.

14 example clauses

Prevailing market rate

The "prevailing market rate" clause refers to a contractual agreement where the payment or pricing is determined based on the current average rate for similar goods or services in the relevant market at the time of the transaction or service. This clause ensures that the pricing remains fair and competitive by aligning with existing market conditions, accommodating fluctuations over the duration of the contract.

12 example clauses

Analyze your contracts. Extract important clauses.

Try our AI contract analysis and extract important clauses and information from existing contracts.

Save your favourite clauses

Insert directly with a single click

Upload preferred precedents