A "bill and hold" clause is a contractual agreement where a seller invoices a buyer for goods but retains physical possession of the goods until a later date. Typically used when the buyer is not ready to take delivery, this arrangement allows the seller to recognize revenue despite the delay in transfer of goods.

Table of Contents

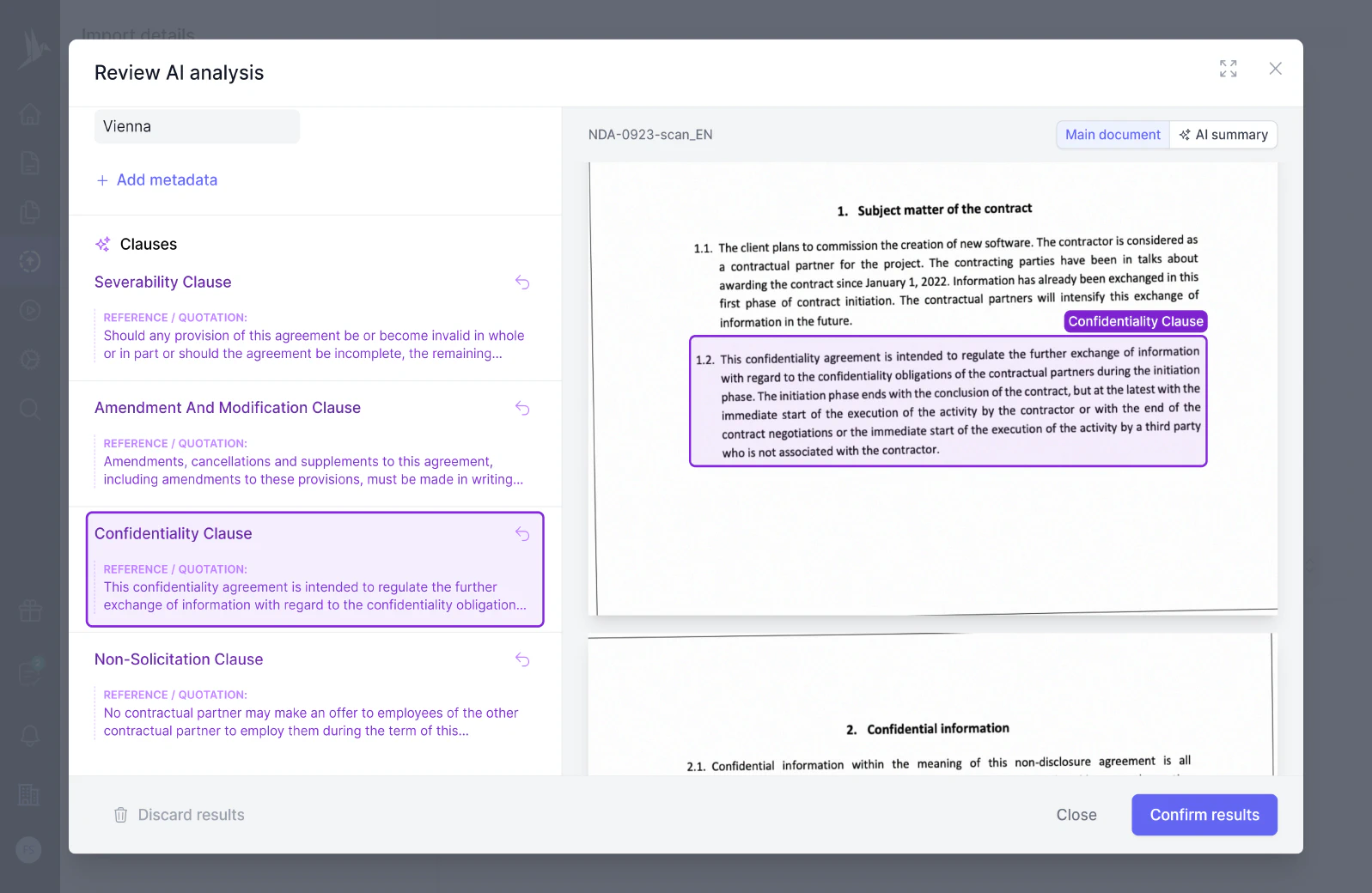

Want to automatically extract clauses from your contracts?

On October 11, 2018, the SEC issued a second subpoena related to the Company’s Value Lighting and All-Around Lighting divisions. The Audit Committee commenced an investigation to examine certain revenue recognition practices at those divisions, specifically the booking of revenue using “bill and hold” accounting for certain transactions occurring from 2014 through 2018. Upon satisfaction of specific requirements imposed by accounting principles and interpretations of the SEC staff, bill and hold revenue accounting permits a company to record revenue for products customers have agreed to purchase that it has segregated for delivery within the company’s own warehouse. Absent satisfaction of these requirements, revenue recognition generally should occur upon delivery of products to customers.

The Audit Committee again retained counsel and forensic accounting consultants in connection with its investigation. The investigation team conducted an extensive review of emails and other documentation, interviewed current and former employees of the Company and analyzed the documentation underlying a subset of the Company’s bill and hold transactions. The Audit Committee and its advisors met regularly between November 2018 and May 2019.

As previously disclosed, on December 10, 2018, the Audit Committee, upon the recommendation of the Company’s management, concluded that, as a result of apparent errors related to revenue recognition associated with bill and hold transactions identified in the course of the Audit Committee investigation, the Company’s consolidated financial statements as of and for each of the following fiscal periods should no longer be relied upon:

•

the fiscal quarters ended March 31, 2018 and June 30, 2018;

•

the fiscal year ended December 31, 2017 and each fiscal quarter therein;

•

the fiscal year ended December 31, 2016 and each fiscal quarter therein; and

•

the fiscal year ended December 31, 2015 and each fiscal quarter therein.

On May 7, 2019, upon the recommendation of the Company’s management and as a result of additional information regarding errors related to bill and hold revenue recognition analyzed during the course of its investigation, the Audit Committee concluded that the Company’s consolidated financial statements for the fiscal year ended December 31, 2014 and the related reports of RSM on such consolidated financial statements and internal control over financial reporting for the fiscal year ended December 31, 2014 should also no longer be relied upon.

The Company did not meet all of the accounting criteria for recognizing revenue on a bill and hold basis from 2014 through the second quarter of 2018 and, thus, certain of its revenues during this timeframe were not recognized in the proper period.

The Company had a material weakness in internal controls with respect to revenue recognition from bill and hold transactions. The Company has retained independent consultants to further assess and propose additional improvements to its controls, which the Company expects will be assessed by the Company’s auditors in connection with the Restatement (as defined below).

Part of the Company’s policy was that signed bill and hold agreements were to be obtained from the customer prior to booking revenue. The Vice President of Sales at Value Lighting frequently did not obtain all signed agreements in a timely manner. He will be terminated from employment following a 90-day transition period.

29. To achieve PSI’s revenue targets, Winemaster, Needham and Davis caused PSI to fraudulently recognize revenue for purported sales of products that the customer had not yet agreed to accept; that had not yet been completed to customer specifications; and for which Winemaster, Needham and Davis had negotiated improper “bill and hold” arrangements. They also caused PSI to improperly recognize revenue for transactions for which they had created undisclosed side agreements that included contingencies such as product return rights and special financing and payment terms. In addition, they caused PSI to improperly recognize revenue in amounts that exceeded the actual sale price. This misconduct began in the fourth quarter of 2014 and increased in scope as the demand for PSI’s product slowed throughout 2015.

31. In the fourth quarter of 2014, PSI appeared to meet the consensus analyst expectation for net revenue of $103.4 million when it reported net revenue of $103.9 million. In that quarter, PSI recognized approximately $846,000 of revenue for a fraudulent bill and hold transaction with Customer A as described below. If PSI had accounted for that transaction in accordance with GAAP, PSI would have missed the consensus analyst net revenue expectation for that quarter by approximately $400,000. Davis approved this fraudulent “bill and hold” transaction.

35. PSI recognized approximately $846,000 of revenue associated with this transaction in the fourth quarter of 2014. PSI recognized revenue on the transaction despite not meeting the criteria required by ASC 605-10-25-1 and which were included in its own policies as described in ¶ 15. Customer A did not request the bill and hold nor did it have a business purpose for ordering on a bill and hold basis. In addition, by reimbursing Customer A for the storage of these engines until Customer A needed the engines in 2015, PSI did not meet the delivery requirements to recognize revenue in 2014.

36. Davis did not tell PSI’s accounting department that the customer did not request the bill and hold, had received extended payment terms, or that PSI was covering the costs of storing the engines. When challenged by a senior operations executive about the appropriateness of recognizing revenue under these circumstances, Davis lied to that executive by falsely telling him that PSI’s CFO and others in accounting had been informed about the transaction details and approved of the accounting for the transaction.

“Eligible Bill and Hold Accounts” means and includes each Account of each Borrower which conforms to the following criteria: (a) an Account that arises with respect to goods that have been sold but not delivered to an Account Debtor on a bill-and-hold basis and the Borrower has received an agreement in writing from the Account Debtor, in form and substance satisfactory to Lender, confirming the unconditional obligation of the Account Debtor to take the goods related thereto and pay such invoice; (b) merchandise or services shall not have been repossessed, returned, rejected or disputed by the Account Debtor and there shall not have been asserted any offset, defense or counterclaim; (c) continues to be in full conformity with the representations and warranties made by any Borrower to Lender with respect thereto; (d) Lender is, and continues to be, satisfied with the credit standing of the Account Debtor in relation to the amount of credit extended; (e) there are no facts existing or threatened which are likely to result in any adverse change in an Account Debtor’s financial condition; (f) is documented by an invoice in a form approved by Lender and shall not be unpaid more than ninety (90) days from invoice date;

“As a result of the material weaknesses previously disclosed, insufficient evidence existed to support the recognition of revenue in arrangements containing bill and hold provisions. Therefore, we deferred the related revenue until product shipped from our warehouse. In connection with the remediation of those material weaknesses, we are now able to support earlier revenue recognition for bill and hold arrangements. Disregarding this benefit, adjusted EBITDA increased 70% in 2019 and our plan reflects at least 15% growth in 2020, excluding the impact from COVID-19,” said Don Pearson, Chief Financial Officer.

Adjusted EBITDA was $15.5 million in the fourth quarter of 2019, compared to $(0.2) million in the fourth quarter of 2018. Fourth quarter 2019 adjusted EBITDA includes $2.8 million of incremental adjusted EBITDA on bill and hold arrangements, as discussed below. Full year adjusted EBITDA was $49.0 million, an increase of 80% compared to the full year 2018.

As previously disclosed in its prior filings with the SEC, including its Form 8-K filed on June 20, 2019, the Company is cooperating with an ongoing investigation by the Securities and Exchange Commission (the “SEC”) relating in part to the manner in which the Company recognized revenue on “bill and hold” transactions. The Audit Committee of the Company’s Board of Directors (the “Audit Committee”) conducted an investigation, the focus of which was to review the extent to which the Company incorrectly recognized revenue with respect to bill and hold transactions. The investigation found, among other things, that the Company did not meet all of the accounting criteria for recognizing revenue on a bill and hold basis from 2014 through the second quarter of 2018 and, thus, certain revenues during this timeframe were not recognized in the proper period.

“Bill and hold” sales generally are sales meeting specified criteria under U.S. generally accepted accounting principles (“GAAP”) to recognize revenue at the time title to goods is transferred to the customer, even though the seller does not ship the goods to the customer until a later time. In typical sales transactions other than those accounted for as bill and hold, title to goods is transferred to the customer at the point of shipment or delivery. As a result of a review concerning the Subject Periods, conducted with the assistance of independent advisors, the Audit Committee identified numerous instances where bill and hold transactions did not appear to meet the requirements for revenue recognition under GAAP. As a result, the Audit Committee has concluded that, in most such cases, revenue should not have been recognized until a later time when the products were subsequently shipped to the customer. As a result, the revenue and the related cost of goods sold reported by the Company for each of the Subject Periods does not accurately reflect the revenue earned in such periods.

As previously disclosed in its prior filings with the Securities and Exchange Commission (the “SEC”), the Company is cooperating with an ongoing investigation by the SEC relating in part to the manner in which the Company recognized revenue on “bill and hold” transactions. The Audit Committee of the Company’s Board of Directors (the “Audit Committee”) conducted an investigation, the focus of which was to review the extent to which the Company incorrectly recognized revenue with respect to bill and hold transactions. The investigation found, among other things, that the Company did not meet all of the accounting criteria for recognizing revenue on a bill and hold basis from 2014 through the second quarter of 2018 and, thus, certain revenues during this timeframe were not recognized in the proper period.

The Company did not consider the provisions in ASC 606-10-55-83 and 84, as none of Bel’s customer-designated hub arrangements meet the definition of a bill-and-hold arrangement. In accordance with ASC 606-10-55-81, “a bill and hold arrangement is a contract under which an entity bills a customer for a product but the entity retains physical possession of the product until it is transferred to the customer at a point in time in the future.”

Although these agreements are not typical bill and hold arrangements, since it appears billing for products only occurs after the customer obtains physical possession, explain if and how you considered the provisions in ASC 606-10-55-83 and 84, including whether you may be providing custodial services that should be identified as a separate performance obligation.

Bill and hold is a sales arrangement where a seller bills a customer for goods but retains physical possession of the products until a later date. This setup generally arises when a buyer is not ready to take delivery of the goods for various reasons, such as lack of storage space or delays in the production of their product that the goods will be a part of. In such scenarios, the seller agrees to “hold” the goods until the customer requests delivery, although the transaction is considered complete for accounting purposes.

When should I use Bill and Hold?

Bill and hold arrangements should be used when it meets the specific revenue recognition criteria set by accounting standards. Key conditions include:

Substantial Reason for the Arrangement: There must be a legitimate reason for holding the inventory on behalf of the buyer, not merely for the seller’s convenience.

Risks of Ownership & Payment Obligation: The buyer must take on the risks of ownership and have an obligation to pay for the goods.

Scheduled Delivery: A fixed delivery schedule should be established to ensure that control over the goods has effectively passed to the buyer.

Separate Identification & Storage: The goods must be separately identified and ready for physical transfer.

Companies often utilize bill and hold when there’s a strategic or contractual agreement with customers about deferred delivery or when managing seasonal sales.

How do I write Bill and Hold?

When documenting a bill and hold arrangement, the agreement should be thoroughly detailed and typically must include:

Buyer’s Request: Clearly state that the arrangement has been made at the buyer’s request and for their benefit.

Reason for Holding: Specify the reason why goods are being held and why immediate delivery is deferred.

Obligation of Payment: Outline the buyer’s obligation to pay and the conditions under which this obligation exists.

Terms of Storage: Describe how the goods will be stored, segregated, and insured, ensuring they remain identifiable.

Scheduled Delivery: Include a specific delivery timeline.

Risks of Ownership: Clarify when and how the buyer assumes risks and rewards of ownership.

These points should be clearly articulated either in the sales contract or as a separate written agreement specifically addressing the bill and hold terms.

Which contracts typically contain Bill and Hold?

Bill and hold provisions are typically found in:

Long-term Supply Contracts: Where arrangements need to account for production schedules aligning with delivery.

Seasonal Sales Agreements: Often seen in industries where timing of delivery is crucial, such as fashion and consumer electronics.

Customized Product Orders: Where goods are made to order and may require storage until the customer is ready for delivery.

Large Equipment Purchases: Frequently used in transactions involving multi-million dollar machinery where buyer’s operational timelines dictate delivery.

It’s crucial that such contracts are detailed and meet the accounting standard requirements to ensure rightful revenue recognition and audit compliance.

More Clauses from the Library

Dive deeper into the world of clauses and learn more about these other clauses that are used in real contracts.

Billing and payment terms outline the specific details regarding the timing, methods, and conditions for invoicing and remittance between parties in an agreement. These terms clarify when payments are due, acceptable forms of payment, any penalties for late payments, and any applicable discounts or incentives for early payments.

A binding arbitration clause requires parties to resolve disputes through arbitration rather than litigation, with the arbitrator's decision being final and legally enforceable. This mechanism aims to provide a more efficient and private resolution process compared to traditional court proceedings.

The "Binding Effect" clause ensures that the terms and conditions of the contract are legally enforceable and extend to the parties involved, as well as their respective heirs, successors, and assigns. This clause guarantees that all parties and their successors must uphold the obligations and rights established in the agreement.

3 example clauses

Analyze your contracts. Extract important clauses.

<

Try our AI contract analysis and extract important clauses and information from existing contracts.